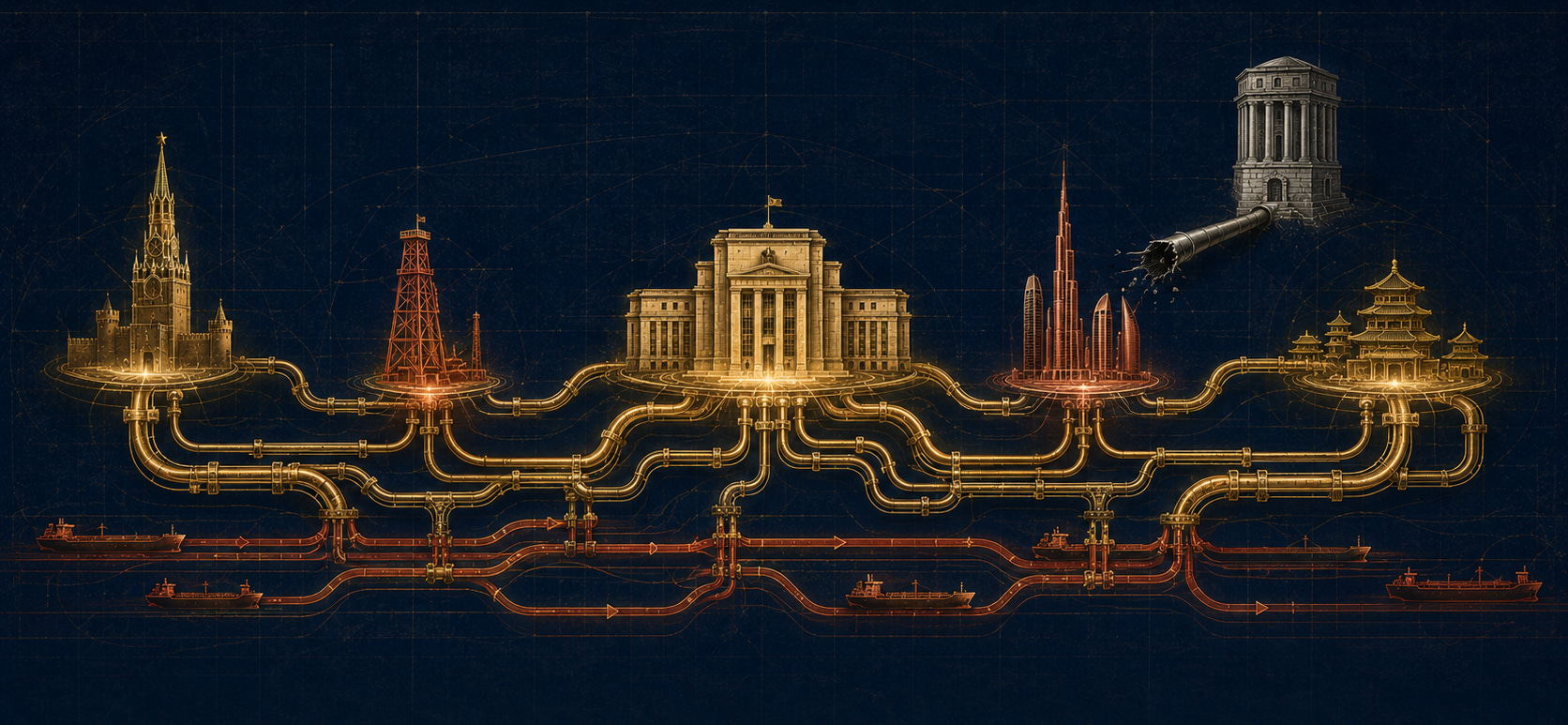

The Settlement Architecture

How a currency event wore the costume of a war!

At 4:48 PM Eastern Time on Tuesday, 12 May 2026, Air Force One lifted off from Joint Base Andrews. President Donald Trump was on his way to Beijing. With him on the manifest were Tim Cook, Elon Musk, the CEOs of Boeing and Citigroup, and Defense Secretary Pete Hegseth. The delegation had been pitched as a trade summit. It was leaving as something else.

Speaking on the South Lawn before boarding, Trump said: “I don’t think we need any help with Iran. We’ll win it one way or another. We’ll win it peacefully or otherwise.” A reporter asked about American gas prices. He answered: “I don’t think about Americans’ financial situation.” Earlier that day, the Energy Department had revised its 2026 average retail forecast to $3.88 per gallon, up from $3.70 the month before. Brent settled at $107.65. WTI at $101.51. The rupee opened at 95.57 and printed a fresh record low of 95.63 in early trade. The arithmetic was running in one direction.

Two days earlier, on the evening of 10 May, Trump had posted to Truth Social: “I have just read the response from Iran’s so-called ‘Representatives.’ I don’t like it, TOTALLY UNACCEPTABLE!” On the morning of 11 May, in the Oval Office, he called the ceasefire on massive life support, Iran’s counter-proposal garbage, and the entire proposal a stupid proposal. He told reporters: “I have the best plan ever.” A large group of generals, he said, was waiting on his word.

He was flying to Beijing without a deal. He was flying to the capital of Iran’s largest customer. And the customer was sending its own foreign minister somewhere else.

Three capitals, two ministers, one architecture

Wang Yi will not be in Beijing on Thursday morning when Trump lands at the host’s side. On 5 May, the Chinese Foreign Ministry quietly conveyed that Wang would be unavailable for the BRICS Foreign Ministers’ Meeting in New Delhi. The Chinese ambassador to India, Xu Feihong, will substitute. The official reason given was scheduling. The simplest explanation is scheduling. The structural explanation is that the BRICS meeting is happening on 14 and 15 May, in New Delhi, on the same two days as Trump’s bilateral with Xi. The piece reads the structural explanation. The simplest explanation cannot be ruled out.

Iran’s Foreign Minister Seyed Abbas Araghchi confirmed on Tuesday that he is travelling to Delhi on Wednesday. Russian Foreign Minister Sergey Lavrov is confirmed. The BRICS ministers from Brazil, South Africa, Egypt, Ethiopia, Indonesia, Saudi Arabia, and the UAE are confirmed. Araghchi will call on Prime Minister Modi on Thursday. Modi will then fly to Abu Dhabi on Friday morning to meet Mohamed bin Zayed before continuing to Europe.

Putin arrives in Beijing the week of 18 May. The Kremlin has not given a date. Vedomosti carries the firmest sourcing, with the week beginning 18 May as the working assumption.

Four leaders. Three capitals. Six days. The choreography is at minimum convenient and at maximum coordinated. Either reading favours Delhi.

Beijing hosts the patron of the old order with no deliverable on the only file that matters. New Delhi hosts the architects of the new settlement layer in the same forty-eight hours. Abu Dhabi receives the third pole as it pivots into its post-OPEC posture. Beijing then hosts Putin, who arrives bearing crude that India and China cannot easily refuse.

A note on what this piece is and is not claiming. The architecture being assembled this week is partial, not complete. The interests of India, China, Russia, Iran, and the UAE overlap selectively rather than identically. The operational maturity of BRICS Pay, CBDC interoperability, and local-currency settlement is uneven and remains substantially below the institutional depth of dollar clearing.

What is being authorised in the next seventy-two hours is political coverage for an FX-conservation ramp under acute external-account pressure, not the launch of a finished alternative settlement system. The piece reads transition pressure, not completed transition. The distinction matters because the two readings have different probability weights, different time horizons, and different ways of being wrong.

What changed in 48 hours

The thesis was that the market was reading a Middle East crisis when the structural event was a currency event. Four data points from the past forty-eight hours moved the thesis from claim to record.

First, Trump killed his own ceasefire in public.

The verbal posture went maximalist while the kinetic posture stayed flat. The Chairman of the Joint Chiefs, General Dan Caine, told reporters on Tuesday that the past week’s exchanges with Iran remained “below the threshold of restarting major combat operations.”

Operation Project Freedom, the US Navy escort effort launched on 4 May, has been paused since 6 May. No B-2 or B-21 deployments have been reported. No carrier surge. No Israeli mobilisation beyond Netanyahu’s CBS interview on 10 May, where he confirmed the war was “not over” and explained the next step as “you go in, and you take it out.”

Trump is talking like a man preparing to bomb and acting like a man preparing to negotiate. He is doing both because he is doing neither. He is heading to Beijing. The structural mismatch between verbal and kinetic posture is what flagged in mid-April: a ceasefire that cannot end the war and a war that cannot resume, suspended by the cost of moving in either direction.

Second, China formally instructed its companies to disobey US sanctions on Iranian oil.

The Ministry of Commerce activated the 2021 anti-sanctions law on 2 May, with implementing regulations finalised on 14 April. Five teapot refiners were named: Hengli Petrochemical (Dalian), Shandong Jincheng, Hebei Xinhai, Shandong Shengxing, and Shandong Shouguang Luqing.

The MOFCOM injunction is the first operational use of the blocking statute. The arrangement now sits in written, regulatory, stated policy. On 12 May, hours before Trump’s departure, the US Treasury added twelve more entities to its sanctions list. Beijing did not blink.

Third, Saudi Aramco’s CEO Amin Nasser quantified the cost.

On Monday 11 May, on the Q1 2026 earnings call, Nasser stated that the market is losing one hundred million barrels of supply every week the Strait of Hormuz remains closed. The net loss to date is approximately 880 million barrels gross.

More than six hundred ships are stuck in the Gulf. The Aramco east-west pipeline has been ramped to seven million barrels per day to bypass Hormuz.

Nasser added: “If the Strait of Hormuz opens today, it will still take months for the market to rebalance, and if its opening is delayed by a few more weeks, then normalization will last into 2027.”

Every week of closed Hormuz transfers one hundred million barrels of demand to alternative supply and alternative settlement. The longer the closure persists, the more institutionally entrenched the alternative architecture becomes. The mechanism is the same one the Actuarial Suez piece set out in early April: a chokepoint priced as a tail risk gets repriced as an operational scenario, and the repricing is permanent regardless of when the strait technically reopens.

Fourth, Modi went to Hyderabad and Somnath on Sunday 11 May and made seven public appeals to Indian citizens.

Use public transport. Reduce cooking oil consumption. Work from home where possible. Avoid foreign travel for one year. Reconsider destination weddings abroad. Conserve foreign exchange. And the heaviest one: avoid buying gold for a year.

A Prime Minister of India publicly asking households to defer gold is the language of a balance-of-payments emergency. The last time this happened was 1991. Kotak and IDFC First are flagging an FY26 BoP deficit between forty and fifty billion dollars. Foreign exchange reserves stand at $703 billion. Global investors have pulled close to $20 billion from Indian equities in the first four months of 2026, more than the full-year record outflow of 2025.

The macro tells one story. The diplomacy tells the same story. Modi flies to Abu Dhabi on Friday to meet the man who controls the dirham peg.

What the settlement layer already is

The settlement architecture is not a future announcement. It is a six-year operational build that is about to receive its political authorisation.

Russia has been settling Indian crude in rupees since 2022. The rupees flow into Russian overseas accounts. From those accounts, the balance is converted into yuan, dirhams, Singapore dollars, and Hong Kong dollars. The mechanism works because the conversion is the bridge over the rupee-trap problem, which is that Russia earns more rupees than it can spend on Indian goods. Yuan and dirham absorb the surplus.

The structure is now standard practice for Indian refiners. This is the operational shadow of the trifurcation The Molecule and the Number traced: paper Brent, Murban physical, and delivered CFR Asia have already become three different commodities. The settlement layer is the fourth split.

Iran has been settling crude in rupees and yuan since the 2019 snapback. The Chabahar payment channel survived sanctions. India transferred operational stake in Chabahar to an Iranian entity in late April 2026, giving Delhi structural deniability while preserving the corridor. Araghchi will be in Jaishankar’s office on Thursday afternoon. He has every reason to leave with something on settlement.

The UAE has had a rupee-dirham local currency settlement framework since July 2023. The first oil deal in INR and AED was signed on 14 August 2023 between ADNOC and IndianOil for approximately one million barrels. The 2023 design coverage target was twenty to twenty-five percent of bilateral trade. The current actual share has not been publicly disclosed by either the RBI or the Central Bank of the UAE, which is itself analytically significant.

The UAE exited OPEC on 1 May 2026. It has signalled to Washington that, in the absence of a bilateral dollar swap line, it could sell oil in yuan. That signal carries structural force. Modi arrives in Abu Dhabi on Friday with India’s rupee at record lows and India’s gold demand officially suppressed. The bilateral has structural urgency on both sides.

China has been settling oil in yuan with Russia since 2022, with Iran since 2019, and with Saudi Arabia in selective tranches since 2023. The MOFCOM blocking statute now extends that posture to Iranian-oil-buying refiners, with state regulatory cover for non-compliance with US Treasury OFAC designations.

BRICS Pay and the BRICS Cross-Border Payments Initiative have been technically operational at pilot scale since 2024. The Reserve Bank of India proposed linking the BRICS member CBDCs (e-rupee, e-CNY, digital ruble, Pix) through a shared messaging protocol in January 2026. Intra-BRICS trade is reported at sixty-five percent in local currencies as of 2024.

The architecture exists. What it has lacked is heads-of-state-level political coverage that turns dispersed bilateral arrangements into a coordinated ramp. That coverage is what the next seventy-two hours will deliver or fail to deliver.

The Bind on Trump

Trump arrives in Beijing in a position that has no precedent since Nixon. He is the patron of the post-1945 order arriving at the capital of the rising power with an unwinnable war in his pocket and an unworkable peace on his desk. All three fogs are operating on him simultaneously.

The sovereignty fog: he does not control Hormuz and cannot reopen it.

The trade fog: his tariff architecture is itself in flux after the February SCOTUS ruling on IEEPA.

The temporal fog: the war is running on Iran’s clock and Xi’s clock, not his. A principal moving inside one fog can navigate. A principal moving inside three fogs is being moved.

He cannot end the war on his terms. Iran’s three demands are conventional: lifting of the maritime blockade, return of frozen assets, and security guarantees against future strikes. Trump has called these terms garbage. Iran has called them reasonable and generous. The asymmetry is in the time horizon.

Iran has the customer base and the storage to outlast the Trump electoral calendar. The US has midterm elections, a rupee at 95.63 reverberating across South Asia, a $3.88 gas price forecast, and an oil major whose CEO has put the supply loss at one hundred million barrels per week into the public record.

He cannot reopen the strait kinetically without expanding the war. The Pentagon’s four options remain on his desk: blockade or invasion of Kharg Island, tanker seizure on the eastern side of Hormuz, large-scale strikes on Iranian enrichment sites, or a return to the late-February campaign at higher intensity. Each of these widens the war. None reopens commercial transit.

A reopened strait requires Lloyd’s underwriters to write war-risk policies on transit. Lloyd’s underwriters require absence of state-actor risk. State-actor risk is the only thing US military action can produce. The decision sits inside the Square Mile, not inside the West Wing.

This is the recursive trap The Toll Is Permanent set out: once a chokepoint becomes a sovereignty question rather than a transit question, kinetic action cannot restore commercial flow.

He cannot accept Iran’s peace proposal without humiliating Israel. Netanyahu has stated, on CBS, that the war is not over while enriched uranium remains in Iran. The Israeli position requires the removal of approximately 970 pounds of 60-percent-enriched material, much of it still believed to be at Isfahan and other sites. Iran has offered to dilute some and store the rest in a third country. Israel rejects the offer.

Trump cannot override Israel without paying domestic political cost. Backing Israel costs him his own ceasefire.

He cannot pivot to Asia while bogged down in the Gulf. CSIS, CFR, and Brookings have all noted the same structural fact in the past week. The Iran war has produced exactly the resource diversion from the Indo-Pacific that Beijing has wanted since 2017. The carrier pinned in CENTCOM is the carrier missing from the South China Sea.

He arrives with the appearance of standing and the substance of dependency. Xi receives him with the appearance of obligation and the substance of patience. The geometry is the one The Captive Holders’ Dilemma named in late April: the principal is bound by the very holders he assumed he commanded.

The Bind on Xi

Beijing’s position is structurally stronger than Washington’s, bit it is not truly unconstrained.

Half of China’s oil and almost a third of its LNG transits Hormuz. Thirteen percent of pre-war oil imports came directly from Iran. Chinese imports through the strait fell from 4.45 million barrels per day before the war to approximately 222,000 barrels per day in April.

The shadow fleet, the teapot refiners, and the Russian backstop have absorbed most of the gap. Russian crude rose from two percent of Indian imports before the Ukraine war to forty-seven percent in March 2026. China’s Russian imports tell a parallel story.

The absorption is not free. Russian crude is sold to China at price discounts that have compressed Aramco’s market share in Asia, which forced the Saudis to cut term prices in February, which accelerated the UAE’s calculation that quota discipline was now a Saudi subsidy worth refusing. Each layer of pressure produced the next.

The UAE’s OPEC exit on 1 May 2026 is the most visible signature of the cascade The Leaking Bucket set out: Saudi Arabia’s fiscal arithmetic is the central pressure on the cartel, and once the bucket leaks, the discipline holding the cartel together leaks with it.

Xi cannot publicly enforce US sanctions on Iran without dismantling the MOFCOM blocking statute he just activated. He cannot publicly defy US sanctions in the joint readout without forcing Trump into a domestic political response. The summit therefore has to produce no joint statement on Iran. The absence of joint language is the deliverable.

The fifth principal of the week is the one not sending a foreign minister anywhere. Saudi Arabia is in a bind that mirrors Washington’s at one remove.

It cannot defect into the BRICS settlement architecture because it remains structurally dependent on US security guarantees.

It cannot stay loyal to dollar pricing because every month of Hormuz closure transfers Asian market share to Russia, to Iran via the teapot refiners, and now to the UAE in its post-OPEC freedom.

Riyadh’s foreign minister will be in Delhi on Friday. Riyadh’s posture will be studious. Saudi Arabia’s silence in the communique is the diplomatic equivalent of the bucket continuing to leak. The architecture moves around the kingdom while the kingdom watches.

The American Calendar

The US has two clocks running on this file. The short clock measures months. The medium clock measures the next eighteen months. Both clocks favour ending the Hormuz problem. Neither clock provides a mechanism for ending it.

The short clock is the gas price clock. The Energy Department raised its 2026 retail forecast to $3.88 on Tuesday. The April CPI print showed gasoline prices up 5.4 percent month-on-month and 28 percent year-on-year. Trump’s own approval rating is at record lows.

The 2026 midterm primaries begin in early March 2027, which means the candidate selection cycle on which the House and a third of the Senate turn is now nine months away. Republican incumbents in suburban districts cannot run on a $3.88 gas price with Hormuz still closed. The Democratic primary field is already test-running the line that Iran was a war of choice that became a war of fuel.

The short clock therefore says: end the war, reopen the strait, deliver the price relief. The short clock has no answer to how.

The four kinetic options on the Pentagon’s desk widen the war and do not reopen Lloyd’s underwriting.

The diplomatic option requires Trump to accept Iran’s terms, which he has called garbage.

The Beijing option requires Xi to deliver Tehran, and Beijing has spent the past two weeks formalising the architecture that makes Tehran independent of any pressure Beijing might apply.

The short clock is loud and demands action. The action set is null.

The medium clock is the dollar architecture clock.

The February SCOTUS ruling on IEEPA was the first crack. The administration’s response (a Section 122 ten-percent global import surcharge, layered Section 301 actions on China, threatened Section 232 expansions) is a tariff regime stitched together from secondary authorities while the primary instrument is in legal abeyance.

The medium clock looks at this and asks the structurally important question: if the President of the United States cannot impose tariffs under the emergency-powers framework that has been the bedrock of presidential trade authority for fifty years, what else cannot he do?

The MOFCOM blocking statute is Beijing’s answer.

The Modi gold appeal is Delhi’s.

The UAE swap-line request is Abu Dhabi’s.

Each is a sovereign actor pricing the medium-clock answer.

The medium clock also reads the federal fiscal cycle.

The next debt ceiling fight arrives in late summer 2026. The Treasury refunding calendar requires foreign captive holders to keep absorbing duration at current scale. Japan’s J-ICS regime, set out in the Captive Holders’ Dilemma piece, binds the largest foreign holder.

The medium-clock vulnerability is that the captive-holder architecture only works if the patron does not push the holders into the alternative architecture. Pushing China to enforce US sanctions on Iran pushes China to formalise its own. Pushing India to stop importing Russian crude pushes India to formalise rupee-rouble-yuan settlement. Each act of pressure produces the structural defection the pressure was meant to prevent.

Trump’s political instinct on the short clock is to escalate. His structural position on the medium clock is to negotiate. The Beijing summit is the venue where the two clocks collide.

The choreography of the visit (Cook, Musk, Boeing, Citigroup on the manifest, AI and rare-earths as the headline deliverables) is designed to make the medium clock look like the short clock. To make a trade summit visible while the actual summit is about whether Beijing will help Washington manage the consequences of a war that Washington started.

The American calendar and the Indian calendar share a shape but run on different deadlines.

The Indian window closes in December 2026, with UP voting in February 2027.

The American window closes in March 2027, when the midterm primaries begin.

India is using the seven months between now and December to build the alternative architecture. The US is using the ten months between now and the primaries to delay the recognition that the alternative architecture is now structural.

The shape is the same. The direction is opposite. The earlier deadline sets the pace, and the earlier deadline is Delhi’s.

The Third Pole

The piece of the week that has been most underweighted in Western coverage is what is happening in New Delhi.

This is the first time since the war began on 28 February that senior Iranian, Emirati, and Saudi officials will be in the same room. The BRICS MENA deputy-ministers meeting on 23 and 24 April in Delhi produced only a chair statement because consensus on West Asia language could not be found. The Foreign Ministers’ meeting on 14 and 15 May will attempt the language again.

A BRICS diplomat told The Quint on 12 May that a joint communique is “doable, but it will require some deft diplomacy.” The trap that produced the April failure is the one Four Clocks: Pakistan’s Structural Trap named in mid-April: Pakistan as the mediator without standing, Iran and the Gulf principals running incompatible timelines, the diplomatic mirage that absorbs effort without producing settlement.

The language that matters in the communique is narrow and specific. Naming of the BRICS Cross-Border Payments Initiative as operational. Reference to CBDC interoperability under India’s chairship. Any mention of local-currency settlement in energy trade. Any reference to secondary sanctions as a concern. Each of these phrases is the operational equivalent of a presidential signature on a treaty that was negotiated under the table.

If the communique carries the language, the architecture is publicly authorised. If it carries only the boilerplate from Kazan 2024 and Rio 2025, the ramp continues underneath while the public signal slips to the Leaders’ Summit in September.

India holds the BRICS chair for 2026. The September summit is in Delhi.

Modi has the calendar he needs to absorb the BoP pain now and stabilise before the next electoral cycle.

The major 2026 Assembly elections concluded with the West Bengal and Assam results on 4 May. The next significant cycle (Goa, Manipur, Punjab, Uttarakhand) arrives in March 2027. The binding deadline sits earlier. Uttar Pradesh, the largest state in the country and the single most consequential Assembly election in the federal calendar, votes in February 2027.

The pain absorption therefore has to be done by December 2026, leaving three months for political posturing and narrative building before the UP vote begins.

The settlement architecture has roughly seven to eight months to ramp from political authorisation to operational scale. The window is the same window inside which the BoP arithmetic has to be absorbed. The rupee is at 95.63. The gas price forecast is rising. The gold appeal is on record.

The Iranian Foreign Minister is in his Foreign Minister’s office. The Russian Foreign Minister is in the same building. The UAE is sending its Foreign Minister or its President’s brother to the same meeting. China is sending an ambassador, which gives Delhi cover to write the language without explicit Chinese fingerprints.

The Russian crude question

A question keeps arriving from readers in the last week. If India is reducing Russian crude purchases under US secondary-sanctions pressure, is India not ceding the architecture before it commits? Are we not losing Russia?

The question conflates three things that need to be separated.

The first is the crude basket composition: where the barrels come from.

The second is the settlement currency: what the barrels are paid in.

The third is the strategic relationship: whether India loses Russia by importing fewer barrels.

On the first, the Indian basket is shifting in April and May. Reuters has reported Indian Oil and HPCL pausing some Russian spot tenders under US secondary-sanctions pressure, while increasing US, Saudi, and UAE term volumes. Russian share of Indian imports has slipped from the 47 percent peak in March 2026 toward the high 30s. This is a tactical concession, not a structural retreat. The basket has always been managed by Indian refiners as a portfolio against four constraints: price, security of supply, transit risk, and diplomatic exposure. The current shift reweights toward Gulf and US suppliers because the transit-risk arithmetic on Russian crude (US secondary sanctions, EU price cap enforcement, shadow-fleet insurance issues) has worsened faster than the price advantage.

On the second, the settlement currency is moving in the opposite direction. Whatever Russian crude India does buy is being settled in rupees, with the rupees converted into yuan, dirhams, and other non-dollar legs through Russian overseas accounts. A smaller volume of Russian crude paid for in zero dollars is structurally more important to the architecture than a larger volume paid for in dollars. The settlement layer is what India is building, not the volume layer.

On the third, India does not lose Russia by reducing crude tonnage. The India-Russia relationship is built on defence (S-400, BrahMos, Su-30 fleet, T-90 upgrades, AK-203 manufacture), on civil nuclear (Kudankulam reactors three through six), on fertiliser (40 percent of Indian DAP and urea imports), on rupee-rouble structural commitments that have absorbed thirty years of trade imbalance, and on a UN Security Council vote that India needs Russia to keep casting. The crude trade is recent, fungible, and replaceable. The defence and nuclear stack is none of those things. Lavrov is in Delhi on Thursday because Moscow understands the difference. Moscow is not in Delhi to extract a crude commitment. Moscow is in Delhi to consolidate the settlement architecture and to coordinate the patron sequence in Beijing the following week.

What looks like ceding from outside is calibration from inside. India is reducing the most exposed leg of the trade (Russian seaborne crude paid in dollars) while expanding the least exposed legs (non-dollar settlement on residual Russian flows, rupee-dirham on UAE flows, rupee-rial on Iranian flows, BRICS Pay on intra-bloc clearing).

The basket gets smaller on Russia. The architecture gets larger on settlement. The relationship gets tighter on defence and nuclear. Three different vectors moving in three different directions, all serving the same FX-conservation logic.

The reader who asks whether India is ceding is reading the wrong column on the spreadsheet. The crude volume column is moving one way. The settlement currency column is moving the other. The strategic relationship column is moving a third way. The architecture is the sum of all three.

The geometry favours announcement. Diplomatic muscle memory favours boilerplate. The reading of Friday’s communique is the single most important interpretive act of the next ten days.

The Abu Dhabi piece

Modi flies to Abu Dhabi on Friday morning. The Ministry of External Affairs has briefed the visit as concerning “bilateral issues, in particular energy cooperation, as well as regional and international issues of mutual interest.” The framing is studiously bland. The context is not.

The UAE exited OPEC twelve days ago. ADNOC’s international vehicle XRG made a 151-billion-dollar bid for US assets in late April. Three Indian citizens were injured in an Iranian strike on a Fujairah oil-processing plant on 5 May, providing political justification for any expansion of India-UAE security and energy cooperation. The strikes have so far stayed below the threshold Bushehr: The Nuclear Threat to the Gulf identified at the end of March, but the threshold is still on the table.

The dirham at Tuesday’s close was Rs 26.07 per AED, the highest ever recorded for UAE-based Indian remitters. The full architecture of the UAE bid was set out in Carrot and Stick and The Triangulation two weeks ago. The Friday meeting is the execution layer.

The joint statement language to watch is sharper than the BRICS communique. Any expansion of the Local Currency Settlement framework. Any specific rupee-dirham crude volume commitment. Any ADNOC equity participation in Indian downstream. Any RBI-CBUAE currency swap line. Any reference to strategic petroleum reserve cooperation.

The UAE has two structurally opposite offers on its desk. From Washington: a bilateral dollar swap line in exchange for staying in dollar pricing on its newly liberated post-OPEC production. From Delhi: rupee-dirham expansion in exchange for crude volume, and implicit yuan optionality through Russian and Iranian triangulation. Sheikh Mohamed bin Zayed is fluent in both languages. The Friday joint statement is the signal of which conversation is heavier this week.

The Settlement Architecture as the structural fact

The architecture is the answer to a question that has been quietly building since 2022. How does the world’s third-largest oil importer pay for crude when the price has doubled, the rupee has hit a record low, and the dollar liquidity layer is itself the strategic vulnerability the US can exploit?

The dollar liquidity layer is not administered from a single point. It is administered across at least eight surfaces: Treasury market depth, Federal Reserve swap lines, correspondent banking networks, derivatives liquidity in New York and London, invoicing conventions in commodity trade, legal enforceability under New York and English law, reserve recycling through sovereign holders, and the underwriting and clearing infrastructure of the Square Mile. The piece The Square Mile set out the legal structure of one of those surfaces: a sovereign zone with its own legal personality that has outlasted every empire and currency regime since the Norman Conquest.

The City is not the whole machine. It is the surface most exposed to the specific mechanism the settlement architecture is engineered to bypass, which is war-risk underwriting and eurodollar clearing on commodity transit. Every settlement-architecture conversation happening in Delhi, Abu Dhabi, and Beijing this week is happening because the principals have learned that being captive to that specific surface is no longer survivable. The architecture does not need to displace dollar hegemony to work. It needs to route around the surfaces where dollar hegemony is most operationally constraining.

The piece The Square Mile: How a Medieval Corporation set out the structure: a sovereign zone with its own legal personality that has outlasted every empire and currency regime since the Norman Conquest. Every settlement-architecture conversation happening in Delhi, Abu Dhabi, and Beijing this week is happening because the principals have learned that being captive to Square Mile clearing is no longer survivable. The architecture is the engineered way out.

The principals are not operating from a shared script. India is pursuing FX conservation, strategic autonomy, energy security, and insulation from sanctions exposure. China is pursuing yuan internationalisation, sanctions resistance, and structural pressure on trade corridors. Russia is pursuing commodity monetisation and escape valves from financial isolation. Iran is pursuing survival liquidity. The UAE is pursuing optionality, post-OPEC manoeuvrability, and capital centrality independent of any single patron.

These vectors intersect at the settlement layer because the settlement layer is the cheapest mutual gain available to all five. They do not intersect anywhere else with similar clarity. The architecture exists where the interests overlap. It thins out where they diverge, and they diverge on most things that are not crude payments.

The answer is that India does not need to find dollars for one hundred percent of its crude basket. It needs to find dollars for the residual after rupee-rouble-yuan, rupee-rial, rupee-dirham, and BRICS Pay clearing have absorbed the rest. The architecture is a dollar-conservation programme.

The distinction between dollar-conservation and de-dollarisation is the difference between an FX management tool and an ideological project. Modi’s seven appeals in Hyderabad were an FX management tool. The BRICS communique on Friday will be an FX management tool. The Abu Dhabi joint statement on Friday will be an FX management tool.

The architecture works in proportion to how much of the crude basket it can move off the dollar leg. The thesis is that a twenty-five to thirty percent non-dollar routing during the Hormuz window is enough to hold the rupee inside the 95 to 100 range without requiring further RBI reserve drawdown. The rupee does not need to find 100. The settlement architecture absorbs the marginal demand.

The market is still reading this as a Middle East crisis. The market is wrong. The market will be right by Monday morning.

Three readouts to watch

The three pieces of paper that will determine whether the architecture commits or stalls are now visible on the diplomatic calendar.

First, the Trump-Xi readout on Friday 15 May. The absence of a joint statement on Iran is the base case. Confirmation of the base case is the structural signal that Beijing has refused to enforce US sanctions. Any explicit mention of Iran in a US-side readout that is absent from the Chinese-side readout is the same signal at lower volume. Any joint language scrubbing the Chinese MOFCOM blocking statute would be the revision-forcing event that takes the architecture off the table.

Second, the BRICS Foreign Ministers’ communique from Delhi on Friday 15 May. Watch for BCBPI, CBDC interoperability, local-currency settlement, secondary sanctions. Watch for the absence of West Asia language, which would itself be a signal that Iran and the UAE could not agree, which would slow the architecture by months.

Third, the Modi-MBZ joint statement from Abu Dhabi on Friday 15 May. Watch for rupee-dirham expansion, ADNOC-IndianOil equity, RBI-CBUAE swap, strategic petroleum reserve.

Three documents. One day. The rupee opens for the new week on Monday 18 May. The first full session after the three readouts is the cleanest market-priced read of whether the architecture commits.

The state of play

Brent is at $107.65 and rising. WTI is at $101.51. The rupee is at 95.63 and the next leg of crude up does not get absorbed in the spot rate. Aramco’s CEO has put the supply loss at one hundred million barrels per week and the normalisation horizon at 2027. China has formally instructed its companies to disobey US sanctions.

The US Energy Department has raised its retail gasoline forecast to $3.88. Trump has called his own ceasefire garbage and has departed for Beijing with Tim Cook, Elon Musk, and Pete Hegseth on the manifest. Putin arrives in Beijing next week. Lavrov and Araghchi arrive in Delhi tomorrow. Modi flies to Abu Dhabi the day after.

The market is pricing a war that has not resumed and a peace that will not arrive. The architecture is pricing what it has always priced, which is the residual.

The Fragmentation Premium clears at whatever Delhi says on Friday and whatever Beijing fails to say on the same day. The variables are how visible the architecture becomes and how fast it scales. The arithmetic runs in one direction.

The molecule is in the strait. The number is in the readout. The settlement is in the silence.

Vedanjanam (Nilmadhab Prasad Sahi) writes on geopolitical structure and the financial architecture of the post-1945 order at vedanjanam.substack.com

🙏👍

Uff, what writing sirji. I think this is your best article just because I understood nearly everything and got a deep sense of satisfaction from understanding something really complex.